|

|||||||||||||||||||||||||||||

|

Scott Bilker is the founder of DebtSmart.com and author of the best-selling books, Talk Your Way Out of Credit Card Debt, Credit Card and Debt Management, and How to be more Credit Card and Debt Smart. Receive the 5-Year Loan Spreadsheet when you subscribe to his email newsletter. |

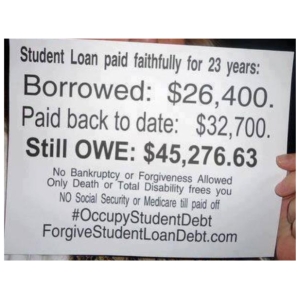

I saw this graphic on Facebook and was taken aback by how expensive this debt seems to be. However, doing the math reveals that the numbers are very misleading.

The graphic says, “Student loan paid faithfully for 23 years: Borrowed $26,400. Paid back to date: $32,700. Still OWE: $45,276.63. No Bankruptcy of Forgiveness Allowed. Only Death or Total Disability frees you. NO Social Security or Medicare till paid off.”

Let’s look at the numbers….

23 years of $32,700 total paid is equal to $118.48 per month.

($32,700/(23×12)=$118.48)

Present Value of the loan is $26,400 (borrowed amount).

Future Value of loan is $45,276.63 (balance after 23 years or 276 months).

Using my financial calculator (Texas Instruments BA-35) and DebtSmart 30-year Loan Worksheet. The APR (Annual Percentage Rate) for this loan turns out to be 6.699%. You can see the entire amortization of this loan here showing all the numbers that prove that rate to be accurate. (Page 8, payment month #276 is 23 years.)

The reason there is so much owed after 23 years is because the monthly payment didn’t cover the interest costs. The interest alone on month #1 is $147.37, however, payments of only $118.47 per month were made, and therefore, the loan will NEVER be paid off. The balance will continue to grow forever. To be more extreme, it’s like buying a car for $1,000 and only paying $1 per month and then complaining after 23 years that you now owe $10,000.

Then there is the matter of what the rates were back in 1990 when this loan was supposedly taken. According to FinAid.org, the interest rates on student loans were fixed at 8%. So how is it possible that the average rate of the claimed loan is 6.699%? In other words, how is it that they paid less than 8%?

Well, one answer is that the government reduced the rate. So not only did they lend this student the money, allow them to make payments far less than needed to pay off (probably to help the borrower out with cash flow), but they also reduced the rate over the 23 years.

The final analysis, as I see it, is that the graphic is either: (1) A complete lie; or (2) The result of getting too many breaks and not being responsible with the loan. Probably the former.

| This entry was posted in Math and Money, Student Loans. Bookmark the permalink. Read more articles by Scott Bilker. (Also see articles by all authors and articles in all categories.) |

Facebook Comments

|

||||||||||||||||||||||