|

Mortgage Minder 3.1 for DebtSmart®

by Chuck Warrix

What

it can do for you!

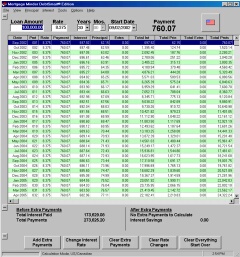

Mortgage Minder is a software package for Windows designed to help you

calculate the right amount to send as an extra principal payment. With

Mortgage Minder, you can try several scenarios and see instant feedback to

help you decide what plan is right for you. In addition, once you start

sending extra payments, you can use Mortgage Minder to track your progress

by updating your saved data file monthly. You can even print reports if you

prefer reading the data in printed format. Mortgage Minder 3.1 new for 2002

now supports Canadian mortgage calculations and variable interest rates. Mortgage

Acceleration Primer

Amortization Schedules

When a mortgage originates, the amount to be borrowed, the interest rate and

term are defined in an agreement between the mortgage company and the

borrower. With this information the mortgage company calculates the amount

of the payment. After the payment is calculated, they can then calculate an

amortization schedule. The amortization schedule is simply a schedule of

principal and interest payment amounts. The following is a sample portion of

an amortization schedule generated by Mortgage Minder. This schedule was

based on a 100,000 dollar loan at 9.5 percent for 30 years.

| Pmt |

Date |

Pmt Amt |

Prin |

Int |

Tot. Prin |

Tot. Int |

Balance |

| 1 |

Oct96 |

840.85 |

49.19 |

791.67 |

49.19 |

791.67 |

99,950.81 |

| 2 |

Nov96 |

840.85 |

49.58 |

791.28 |

98.76 |

1,582.94 |

99,901.24 |

| 3 |

Dec96 |

840.85 |

49.97 |

790.88 |

148.73 |

2,373.83 |

99,851.27 |

| 4 |

Jan97 |

840.85 |

50.37 |

790.49 |

199.10 |

3,164.32 |

99,800.90 |

| 5 |

Feb97 |

840.85 |

50.76 |

790.09 |

249.86 |

3,954.41 |

99,750.14 |

| 6 |

Mar97 |

840.85 |

51.17 |

789.69 |

301.03 |

4,744.10 |

99,698.97 |

| 7 |

Apr97 |

840.85 |

51.57 |

789.28 |

352.60 |

5,533.38 |

99,647.40 |

| 8 |

May97 |

840.85 |

51.98 |

788.88 |

404.58 |

6,322.26 |

99,595.42 |

| 9 |

Jun97 |

840.85 |

52.39 |

788.46 |

456.97 |

7,110.72 |

99,543.03 |

| 10 |

Jul97 |

840.85 |

52.81 |

788.05 |

509.77 |

7,898.77 |

99,490.23 |

| 11 |

Aug97 |

840.85 |

53.22 |

787.63 |

563.00 |

8,686.40 |

99,437.00 |

| 12 |

Sep97 |

840.85 |

53.64 |

787.21 |

616.64 |

9,473.61 |

99,383.36 |

Take a look at the first payment,

particularly the "Payment", "Principal" and

"Interest" columns. Out of that 840 dollar payment only 49.19 was

applied towards the principal amount of the loan. This means that after the

840.85 payment, the amount owed is still 100,000 minus 49.19 or 99,950.81 as

shown in the "Balance" column. Now notice the rest of the payments

and the way they are broken down. The payment stays the same, but the

principal and interest amounts change. Each payment, the principal amount

increases and the interest amount decreases. That is because the interest is

calculated on the remaining unpaid balance of the loan, which is constantly

being reduced (ever so slightly in the beginning) by the principal amount of

the payment. At some point the principal amount of the payment will be more

than the interest amount. One would think that this point would be the

middle of the term, or in this case around the 180th payment. This is not

true. In fact, with this loan the principal amount of the payment exceeds

the interest amount around the 273rd payment. See for yourself.

| Pmt |

Date |

Pmt Amt |

Prin |

Int |

Tot. Prin |

Tot. Int |

Balance |

| 271 |

Apr19 |

840.85 |

413.53 |

427.33 |

46,435.41 |

181,436.08 |

53,564.59 |

| 272 |

May19 |

840.85 |

416.80 |

424.05 |

46,852.21 |

181,860.14 |

53,147.79 |

| 273 |

Jun19 |

840.85 |

420.10 |

420.75 |

47,272.31 |

182,280.89 |

52,727.69 |

| 274 |

Jul19 |

840.85 |

423.43 |

417.43 |

47,695.73 |

182,698.32 |

52,304.27 |

| 275 |

Aug19 |

840.85 |

426.78 |

414.08 |

48,122.51 |

183,112.39 |

51,877.49 |

| 276 |

Sep19 |

840.85 |

430.16 |

410.70 |

48,552.67 |

183,523.09 |

51,447.33 |

| 277 |

Oct19 |

840.85 |

433.56 |

407.29 |

48,986.23 |

183,930.38 |

51,013.77 |

| 278 |

Nov19 |

840.85 |

437.00 |

403.86 |

49,423.23 |

184,334.24 |

50,576.77 |

| 279 |

Dec19 |

840.85 |

440.45 |

400.40 |

49,863.68 |

184,734.64 |

50,136.32 |

| 280 |

Jan20 |

840.85 |

443.94 |

396.91 |

50,307.63 |

185,131.55 |

49,692.37 |

| 281 |

Feb20 |

840.85 |

447.46 |

393.40 |

50,755.08 |

185,524.95 |

49,244.92 |

This is also almost the point where half of

the loan is paid. That means it would take you over 23 years to pay off the

first half this loan, which means the other half is paid in a little over 7

years! Now look at the end of this loan.

| Pmt |

Date |

Pmt Amt |

Prin |

Int |

Tot. Prin |

Tot. Int |

Balance |

| 349 |

Oct25 |

840.85 |

764.94 |

75.92 |

91,175.29 |

202,282.83 |

8,824.71 |

| 350 |

Nov25 |

840.85 |

770.99 |

69.86 |

91,946.28 |

202,352.69 |

8,053.72 |

| 351 |

Dec25 |

840.85 |

777.10 |

63.76 |

92,723.37 |

202,416.45 |

7,276.63 |

| 352 |

Jan26 |

840.85 |

783.25 |

57.61 |

93,506.62 |

202,474.06 |

6,493.38 |

| 353 |

Feb26 |

840.85 |

789.45 |

51.41 |

94,296.07 |

202,525.47 |

5,703.93 |

| 354 |

Mar26 |

840.85 |

795.70 |

45.16 |

95,091.77 |

202,570.62 |

4,908.23 |

| 355 |

Apr26 |

840.85 |

802.00 |

38.86 |

95,893.76 |

202,609.48 |

4,106.24 |

| 356 |

May26 |

840.85 |

808.35 |

32.51 |

96,702.11 |

202,641.99 |

3,297.89 |

| 357 |

Jun26 |

840.85 |

814.75 |

26.11 |

97,516.86 |

202,668.09 |

2,483.14 |

| 358 |

Jul26 |

840.85 |

821.20 |

19.66 |

98,338.05 |

202,687.75 |

1,661.95 |

| 359 |

Aug26 |

840.85 |

827.70 |

13.16 |

99,165.75 |

202,700.91 |

834.25 |

| 360 |

Sep26 |

840.85 |

834.25 |

6.60 |

100,000.00 |

202,707.51 |

0.00 |

The payments are still the same, but the

principal and interest amounts have switched places. Now the majority of the

payment is showing in the principal column and the smaller amount in the

interest column. Again, this is because the interest is calculated on the

unpaid amount of the loan. Toward the end of the loan, the unpaid amount is

smaller therefore the amount of interest paid for those payments is smaller

as well.

Mortgage Acceleration

The idea of mortgage acceleration is to pay an additional amount towards the

principal portion of the loan to reduce the principal and reduce the amount

of interest charged for the next payment cycle. I think you will be

surprised when you see the difference that just a few dollars each month can

make.

Using the same loan as an example, would you

believe that you can save over FIFTEEN THOUSAND dollars over the term of the

loan by sending only 10 dollars a month extra with your payment! You will

also cut 1.75 years or 22 payments off the term of the loan. If you pay an

extra 25 dollars each month, you save almost 33,000 dollars in interest and

cut the term to 26 years! How about 100 dollars extra each month? You'll

save over 80,000 dollars in interest and pay the loan off 10 years early!

Now for the trick question of the day. The

normal payment for this loan is 840 dollars. How much do you think you would

have to send each month in order to pay the loan off in half the normal

term? Double the payment to 1680 dollars? Maybe a little less? Would you

believe that if you paid an extra 205 dollars each month, you will pay this

loan off in 15 years!! And in the process, save over 115,000 dollars in

interest! YES, that IS 115 THOUSAND dollars! Are you ready to you get

started?

Get Started Now! (this is very important)

Now all you have to do is decide how much you can send each month. Decide

now and get started right away. The longer you wait, the more money you

could have saved. For example, if your loan was like the example we have

used throughout this document, you will save almost 83,000 dollars by paying

just 100 dollars extra each month, IF you start with the first payment. Now

what if you waited a year or two and then started the extra payments? Well,

if you started the extra payments on the second year, you will still save

over 76,000 dollars. So that means the extra 1200 dollars in payments that

you would have made the first year would have been worth 7,000 in interest

savings. If you wait until the second year, your savings drop to just under

71,000 dollars, which is still good, but not as good as if you start with

the first payment. The point here is to get started as soon as possible. The

sooner you start, the more you will save.

|